Iris Software Perspective Paper

Real-world Asset Tokenization Can Transform Financial Markets

Integration with Distributed Ledger Technologies is critical to realizing the full potential of tokenization

Integration with Distributed Ledger Technologies is critical to realizing the full potential of tokenization.

Thank you for reading

Ashwani Kumar, Principal Architect at Iris Software

Subramanian Viswanathan, Associate Vice President - Financial Services Practice at Iris Software

Vishwas Tomar, Associate Director - Automation Practice at Iris Software

The global financial markets create and deal in multiple asset classes, including equities, bonds, forex, derivatives, and real estate investments. Each of them constitutes a multi-trillion-dollar market. These traditional markets encounter numerous challenges in terms of time and cost which impede accessibility, fund liquidity, and operational efficiencies. Consequently, the expected free flow of capital is hindered, leading to fragmented, and occasionally limited, inclusion of investors.

The wealth management industry, dedicated to constructing and overseeing portfolios for affluent and high net worth individuals, represents a substantial $5 trillion market. The interest in alternative investments, such as private credit, real estate, and private equity, is burgeoning because of the opportunities they offer to diversify portfolios and better manage risk returns.

Many mature investors adopt and avail of these opportunities through different channels. But it remains a challenge to make these options accessible to a broader range of investors.

Illiquid markets with little or no low activity and the absence of a secondary market pose significant obstacles, limiting investment options and hindering diversification and risk management across borders. Regulatory restrictions and reliance on intermediaries worsen the situation, resulting in unclear processes, long transaction times, and higher expenses.

In response to these challenges, today's financial services industry seeks to explore innovative avenues, leveraging advancements such as Distributed Ledger Technology (DLT). Using DLTs, it is feasible to tokenize assets, thus enabling issuance, trading, servicing and settlement digitally, not just in whole units, but also in fractions.

The following sections will delve into understanding tokenization and its potential to overcome the challenges noted earlier. It will discuss the underlying technology, successful use cases, issues associated with implementation, and conclude with our viewpoint.

Imagine a transformative approach that preserves the value and integrity of assets while ensuring transparent, secure transactions. Such a solution would not only solve the challenges noted earlier but also pave the way for a more inclusive and dynamic financial landscape. Asset tokenization is the solution approach being considered actively by many large firms.

Asset tokenization is the process of converting and portraying the unique properties of a real-world asset, including ownership and rights, on a DLT platform. Digital and physical real-world assets, such as real estate, stocks, bonds, and commodities, are depicted by tokens with distinctive symbols and cryptographic features. These tokens exhibit specific behavior as part of an executable program on a blockchain.

The inherent capabilities of DLT facilitate multi-party engagement, multi-asset representation, and the integration of programmability with automated workflows. These have been instrumental in spearheading innovative avenues for asset tokenization, particularly within financial institutions and wealth management firms. These endeavors can experience substantial acceleration with the advancement of operational processing capabilities, the introduction of secondary liquidity through tokenizing fund positions on a shared ledger system, and the provision of detailed reporting and consolidation of fragmented investor ownership registries.

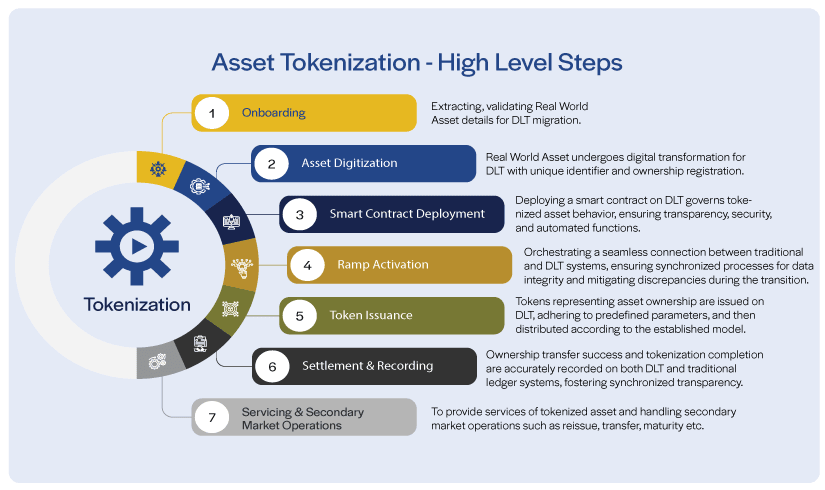

The fundamental elements in tokenization include the asset, the ledger, and the process of tokenization itself. An asset is the tangible real-world object possessing inherent economic value, typically owned by an entity. Examples include stocks and real estate. The ledger serves as the record-keeping system for ownership details. Traditionally, recording has been accomplished using traditional ledgers, which typically consist of two components: a persistent state (DB layer), and rules for accessing and processing assets (application layer). In conventional systems, the reliability of an asset depends on the application operator, typically constrained by legal and regulatory frameworks. Stock exchanges and pension funds are prime examples of application operators.

With the emergence of DLT as a programmable ledger and the introduction of smart contracts, a binding relationship can be established between the data (representing core asset properties) and pre-agreed standards (representing conditional execution logic). These standards can be linked to real-world events associated with a specific token, such as asset locking or maturity condition checks. These assets are now referred to as tokens, serving as representations of real-world assets with built-in transactional logic. They operate without the need for intermediaries, support a wide range of assets not typically available on traditional ledgers, enable fractional ownership, and offer 24/7 availability and high liquidity.

In practical terms, envisioning how a real-world asset can exist on a DLT platform while retaining its value can be challenging, given the entrenched use of traditional systems. Two widely employed methods address this challenge:

a. Asset-Based Tokenization: This method operates on the concept of a digital twin of the traditional asset. The physical asset remains within its parent system, such as a bank ledger or a custodian account. However, it is immobilized in these underlying ledgers, and a digital representation is created on a blockchain as an investor's claim on the asset. This token on the blockchain holds the same value as the asset on the traditional ledger, with all the functionalities supported by a smart contract. Another name for asset-based tokens is security tokens. These also represent ownership of real-world assets. Since these digital assets derive their value from an external asset, they are subject to federal laws governing securities.

b. Native Asset Tokenization: In this approach, the financial instrument itself is issued natively as a smart contract-based token on a blockchain. It encapsulates the inherent contractual rights and obligations without requiring external asset backing. Bonds, equities, fund shares, and various other financial instruments can be represented as native tokens.

Utility Token: Utility tokens create a form of digital coupon redeemable in the future for discounted fees or special access to a product or service. Unlike security tokens, utility tokens are not considered investments and, when properly established, may be exempt from federal laws governing securities.

Many domains, especially financial institutions, have started recognizing the benefits of tokenization and begun to explore this technology. Some of the benefits include:

• Fractional Ownership: Tokens enable fractional ownership of high-value assets. Investors can own a fraction of an asset, making it more accessible to a wider range of entities.

• Increased Liquidity: By enabling secondary trading on compliant security token exchanges, tokens contribute to increased liquidity for traditionally illiquid assets.

• Efficient Transfer of Ownership: DLT enables an efficient and transparent transfer of ownership. It helps reduce the manual intervention and administrative hurdles associated with traditional securities transactions.

• Ownership Representation: Tokens represent ownership or a stake in an underlying asset with owners having legal rights tied to the asset, such as dividends, voting rights, or a share in profits.

• Programmability: Implicit programmability helps automate the token

life-cycle management and any usual operation associated with it.

Every technology innovation comes with its own challenges and risks that have to be overcome before it is fully adopted and becomes a mainstream service. Similarly, asset tokenization, though being adopted and experimented with at a broader level, has its share of challenges. Some of them are:

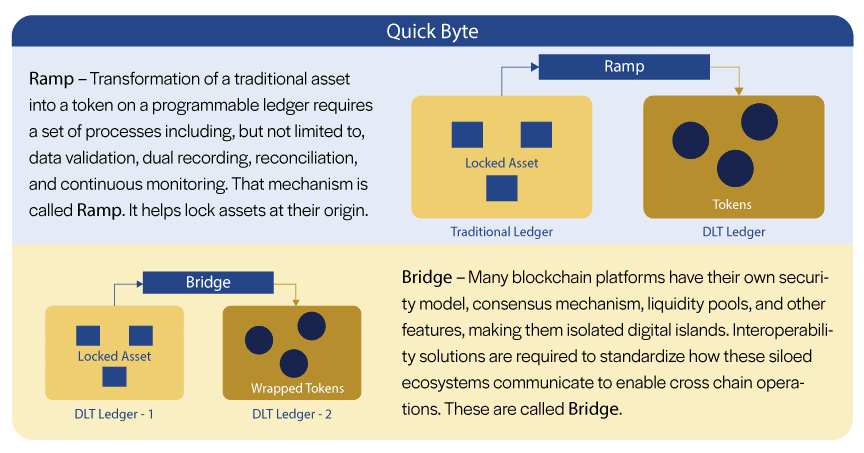

• Absence of Standardization: The lack of industry adopted and accepted standards can hinder interoperability and create challenges in cross-platform transactions. This results in tokens getting locked in disparate and siloed systems. More time may be needed before the true potential can be realized.

• Traditional Systems Integration: There is no set standard for bridging the gap between traditional financial systems and DLT platforms. This often proves to be a complex issue.

• Programming Vulnerabilities: Smart contracts are critical to providing functionality to tokens. But they are not immune to errors or vulnerabilities. As the new systems are not battle-tested like the traditional ones, any flaw in the execution logic can lead to unintended consequences, affecting the performance of tokenized assets.

• Market Fragmentation: The absence of a unified marketplace and the siloed DLT ecosystems can lead to fragmentation. A lack of interoperability may hinder the seamless transfer of assets between different platforms.

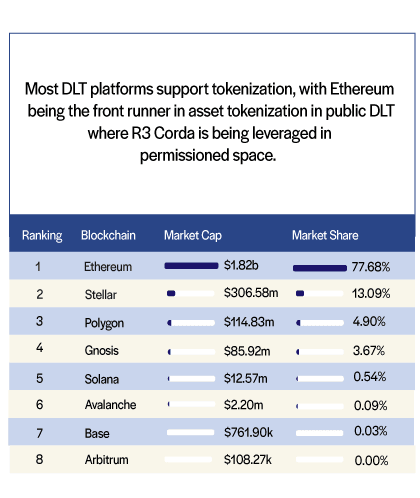

• Technology Risks: Most DLT platforms and technologies are still evolving by learning from mistakes and working on industry feedback. Immutability at times presents a bigger challenge as software updates, protocol changes, or shifts in blockchain consensus mechanisms need to be carefully rolled out.

However, these are still very early days in terms of realizing the full potential of tokenization.

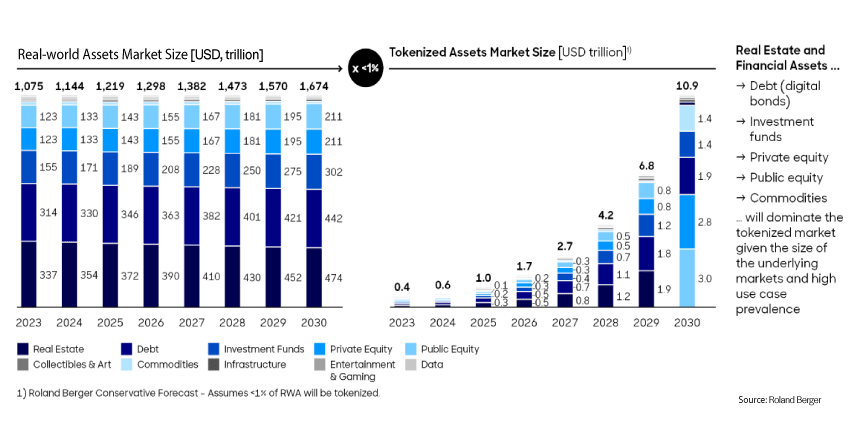

We are now witnessing an upward trend in real-world asset tokenization. According to Roland Berger, the tokenization market will reach close to $10.9 trillion by 2030.

There are certain initiatives, such as Project Guardian, which are exploring asset tokenization using multiple DLT ecosystems, making them interoperable with finely-tuned bridges. This is an example of how multi-ledgers and multi-asset shared ledgers can tokenize assets from traditional legacy systems and provide a seamless workflow that helps portfolio managers expand their horizons in providing investment opportunities to investors.

J.P. Morgan’s tokenization platform, Onyx, has processed over $1 trillion in value since its launch in 2020. Goldman Sachs has launched its digital asset tokenization platform, GS DAP, with the issuance of €100 million ($104 million) digital bond for the European Investment Bank (EIB) on the private GS blockchain. Another example is of Belgium-based financial services company Euroclear, which settled a World Bank bond on the Luxembourg Stock Exchange.

Tokenization is undeniably ushering in a new era of transformation in the functioning of financial markets, particularly in the realm of securitization of assets, and broadening the investment landscape. This paradigm shift has the potential to offer advantages through the automation of transactions and an expansive scope for asset tokenization, ownership, and transfers. However, widespread adoption of such tokenization faces distinct economic, legal, and technical challenges. For instance, they are contingent upon the nature of the asset in question, its physical jurisdiction v. jurisdictions where it could be owned/traded.

With the recent surge in the adoption of tokenization, a diverse array of platforms have emerged, paving the way for broader success, but at the same time creating fragmented islands of ledgers and related assets. As capabilities mature and adoption grows, interconnectivity and interoperability across ledgers representing different institutions issuing/servicing different assets could improve, creating a better integrated market landscape. This would be critical to realizing the promise of asset tokenization using DLT.

Ashwani Kumar, Principal Architect, Iris Software, is the author of the book, Hyperledger Fabric In Depth. Ashwani has considerable knowledge and experience with digital ledger technology (DLT) and blockchain platforms such as Ethereum, Hyperledger Fabric & R3 Corda. As a technology enthusiast, he has successfully developed and delivered numerous large-scale enterprise solutions.

Subramanian Viswanathan, Associate Vice President - Financial Services Practice, Iris Software, is a passionate digital transformation specialist. Subramanian’s expertise includes building end-to-end crypto currency wallets, spanning product management, technical architecture, all phases of implementation, and partnerships with crypto exchanges.

Vishwas Tomar, Associate Director - Automation Practice, Iris Software, Vishwas is responsible for driving the growth of the Automation Practice and development of DLT solution capabilities. Vishwas has excellent command of DLT blockchain technology and is an expert in crafting innovative automation solutions across verticals.

Iris Software has been a trusted software engineering partner to Fortune 500 companies for over three decades. We help clients realize the full potential of technology-enabled transformation by bringing together a unique blend of domain knowledge, best-of-breed technologies, and experience executing essential and critical application development engagements. With over 4,300 skilled professionals, Iris builds mission-critical technology solutions across banking, financial services, insurance, life sciences, logistics, and manufacturing. Iris Automation services and solutions include Intelligent Automation, Quality Engineering, and Low-code No-code development. Click here to read about the milestones of our 30-year journey.

Learn more about our Automation capabilities at:https://www.irissoftware.com/services/automation/

Click here to read about the milestones of our 30-year journey.